According to polling across more than 20 countries highlighted by Politico, respondents in several regions are now more likely to identify China than the United States as the future leader in artificial intelligence. That finding doesn’t match any technical benchmark. That’s precisely the problem.

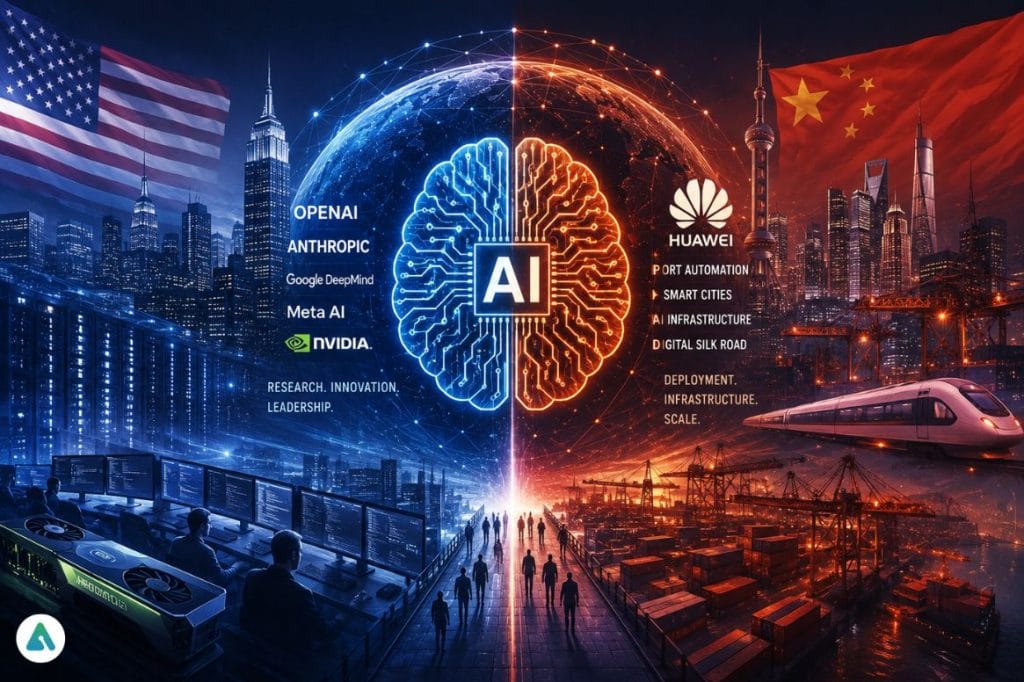

The Stanford HAI AI Index still places the U.S. ahead in research output, model performance, and private investment. NVIDIA dominates advanced AI chips. OpenAI, Anthropic, Google DeepMind, and Meta AI define the frontier. By every measurable capability metric, America leads.

Global perception, in a growing number of markets, is reaching the opposite conclusion.

China isn’t beating the U.S. at AI. It’s beating it at visibility.

While American firms build better models, Chinese companies — led by Huawei — deploy integrated infrastructure. Huawei’s AI-powered logistics and transportation systems now operate across more than 100 ports and 300 urban rail lines spanning 70 cities worldwide. It has launched Arabic-language AI models in Egypt, promoted AI cloud adoption in South Africa backed by its own Ascend chips, and pitched AI processors to government and enterprise partners in the UAE, Saudi Arabia, and Thailand. That’s not a benchmark score. That’s a footprint.

For policymakers evaluating long-term technology partners, footprints outweigh abstractions. A government that has watched Huawei wire its port logistics doesn’t need a white paper to form an opinion on who leads in AI.

Adoption patterns reinforce this. Across several emerging economies, AI feels operational — visible in urban systems, logistics networks, and enterprise software — in ways that feel less visible in many Western markets. Separate surveys by the European Council on Foreign Relations find stronger expectations of Chinese technological influence in countries like Brazil and South Africa than in Western Europe. The directional trend holds across methodologies: perception and technical reality are decoupling.

Export Controls Address Capability. Perception Operates Elsewhere.

Washington’s chip restriction strategy targets China’s ceiling — specifically, limiting access to the advanced GPUs needed to train frontier AI models. The logic is defensible. IDC data shows China’s AI infrastructure investment fell 8.1% year-over-year in Q4 2025 as export controls constrained access to leading-edge accelerators.

But frontier capability and global deployment influence are different games. Countries outside the U.S. alliance structure regularly prioritize cost, implementation speed, and integrated support over access to the most advanced silicon. When American firms face export compliance barriers, the alternative doesn’t need to be better — it needs to be available, bundled, and cheaper. Brookings analysts have noted that China is actively pursuing a complementary strategy: pairing energy infrastructure with AI deployment packages, particularly across the Middle East and Southeast Asia. That combination is hard to match with a chip restriction.

The Forrester analysts who attended Huawei Connect 2025 noted that customers from Latin America, Africa, Europe, and the Middle East cited affordability and reliable deployment partnerships as primary reasons for engagement. The technology didn’t need to be the best. It needed to show up.

The Real Inflection Point Is a Procurement Decision

The AI race no longer runs on a single metric. It spans models, chips, infrastructure, financing, and the kind of long-term integration that makes switching costs prohibitive. The United States leads on the first two. China competes aggressively on all five.

That asymmetry matters because perception gaps compound differently than capability gaps. If governments begin building regulatory frameworks, data infrastructure, and decade-long technology partnerships based on perceived momentum rather than measured performance, influence shifts before the underlying capability gap closes. Standards bodies, procurement cycles, and supply chain architecture don’t wait for benchmark updates.

China’s dependency on external inputs for high-end chip manufacturing hasn’t disappeared. The Federal Reserve’s analysis of global AI computing capacity still shows the U.S. maintaining a leading position through 2026 and beyond. The capability gap hasn’t closed.

But right now, the AI race has a technical leaderboard and a political leaderboard — and they have different leaders.

The question isn’t whether America leads in AI. It’s whether that lead is legible to the countries choosing their next infrastructure partner today.

Related: Wall Street Is About to Find Out What AI Is Really Worth